Addressing Compliance Risk

Why Is This Client in This Portfolio?

Matt Kadnar, Sales Lead, Nebo Wealth

Andy Finnegan, Marketing Lead, Nebo Wealth

Imagine you’re asked by a regulator: “Why is this client in this portfolio?” Many firms can’t confidently answer this question and that’s a compliance problem. Or as one advisor noted, “we have five offices and ten different ways of doing things.

In today’s regulatory environment, compliance risk has become one of the most significant and potentially costly challenges facing advisory firms. With scrutiny from regulators, the standards for documenting portfolio construction, suitability, and ongoing oversight are rising. And for firms with distributed advisor teams, multiple offices, or “rep as PM” structures,1 inconsistent practices can lead to real risk.

One of the most common areas of concern? Portfolio management. In fact, the SEC’s Office of Compliance Inspections and Examinations (OCIE) has observed that more than half of the advisors examined were cited for deficiencies related to portfolio management practices. 2 It’s the kind of thing we hear often: for example, a retired couple in their late 60s and a mid-career tech executive, each with very different goals and time horizons, assigned to the same moderate model. That’s not personalization. That’s a weak spot.

For firm leaders, the implications are serious. When advisors place clients with vastly different financial goals, time horizons, and risk profiles into the same model, or when advisors apply meaningfully different allocations to clients with similar needs, it raises fundamental questions. How are asset allocation decisions made? What is the advisor’s documented rationale? How is the process monitored and supervised across the organization?

Without a consistent, transparent, and repeatable investment process in place, firms face heightened risk on multiple fronts:

- Regulatory enforcement from inadequate suitability

- Regulatory enforcement for inadequate supervision

- Legal liability from client complaints or disputes Reputational damage that can erode client trust and firm value

The Regulatory Lens on Asset Allocation

Asset allocation is one of the most important levers in achieving client outcomes. Advisors agree: we have asked hundreds of advisors to rate the importance of asset allocation on a scale of 1 to 100 and the median response was 92.

Yet despite its importance, asset allocation practices remain inconsistent and often undocumented. Many advisors still rely on:

- Oversimplified risk scores that fail to capture a client’s full financial picture

- One-size-fits-all models that lump 80–90% of clients into the same “moderate” model

- Advisor intuition, which may be valuable but is difficult to scale, supervise, or defend 3

On a scale of 1 to 100, how important is asset allocation in determining client outcomes? 4

92

When an advisor struggles to substantiate why a given client is in a particular model portfolio, they face a compliance problem (and potentially a client relationship problem) that is further magnified when allocating to private assets and their accompanying illiquidity. What firms need is a scalable, auditable way to link portfolio construction to each client’s financial reality, not just a risk score.

We help to solve for this by connecting each portfolio back to a client’s specific goals, time horizon, and risk tolerance and dynamically re-optimizing the portfolio as those goals or market conditions change. This provides firms with a repeatable, documented and auditable rationale for every portfolio decision, across every advisor. In the words of one of our users, “Nebo is simply a better way to frame portfolios in the context of client goals.”

Advisor Autonomy vs. Firm Oversight

For large RIAs, rollups, and aggregators, compliance risk is magnified by complexity. Firms often promise advisor autonomy in recruiting but then struggle to enforce consistent practices. Allowing full discretion (i.e., the “rep as PM” model) across hundreds of advisors can lead to:

- Wide variability in portfolio practices

- Increased operational risk and compliance burden

- Supervisory and due diligence challenges

Adding more model portfolios in response to advisor demands can backfire, leading to a glut of options that are difficult to monitor, validate, and maintain. The answer isn’t more models. It’s a smarter, more systematic way to map clients to the right portfolio.

As one industry report put it, “walking the tightrope of enterprise risk management and advisor autonomy can be difficult, costly, and inefficient. While models may be more HQ- friendly, many top-producers want the freedom they feel they’ve earned. The difficulties … has resulted in a proliferation of advisory programs –along with the operational inefficiencies, inflated headcount, and technical debt required to support them. ” 5

And we’ve heard the same directly from enterprise advisory teams: 6

“The only way to stay safe is to get to a repeatable process the whole team is using.”

“If we adopt one office’s methodology, the others feel like we’re calling them ugly.”

“It’s a challenge for the industry to ensure that the client is still in the right portfolio.”

Indeed, firms are grappling with scalability, suitability, and defensibility:

“We’re looking to fine-tune advice, be more precise vs. [taking a] spaghetti-against-the-wall type of approach to model portfolio selection.”

“We’re guessing. You can say we’re guessing.”

“We have a lot of models; they get overwhelmed.”

“We’re struggling to be scalable on a client-by-client basis.”

And from a regulatory lens, the stakes are rising, especially in decumulation:

“There’s more emphasis now on how advice is delivered for people in decumulation, how sustainable goals and strategies are, and how you tell that story.”

“The real alpha isn’t in beating benchmarks. It’s in building portfolios clients actually stick with.”

“We want to be more precise; document suitability, be more accurate in what we deliver to the client.”

These challenges point to a deeper issue: most firms lack a unified process to guide portfolio decisions across teams, offices, and client types. The result is a patchwork of practices – some thoughtful, others more ad hoc – with no reliable way to supervise, scale, or defend them. The solution is not just to implement tighter controls or add more one- size-fits-all models, but to establish a shared process that empowers advisor flexibility while enabling firm-wide consistency and oversight.

Our process helps solve this dilemma in a scalable framework. Firms can offer advisors flexibility through open architecture while still embedding a consistent, institutional- grade process for model selection or portfolio customization. This creates a better balance between enterprise risk management and advisor independence.

Illiquid Assets: The Next Frontier of Suitability Risk

As private investments become more mainstream in wealth portfolios, they also introduce new compliance risks. Illiquid assets, especially those with drawdown or commit/call structures, require careful planning and liquidity management. Once committed, clients cannot easily adjust their allocation if market conditions or financial needs change. Missteps can lead to defaults, penalties and significant legal exposure.

Regulators have taken notice and are evaluating how advisors assess suitability, and liquidity needs when recommending illiquid investments. 7 As alternatives make up a larger share of client portfolios, the questions becoming increasingly critical for advisors: “why did you allocate this percentage of illiquid assets to this client?” and “what was your decision process?”

A recent CAIS and Mercer survey highlights the pressure many advisors are under. 8 Among the top challenges in adopting alternatives is the difficulty of determining appropriate target allocations, an issue that 21% of respondents flagged. Many advisors are still navigating these decisions without a repeatable framework, relying instead on instinct or back-of-the-envelope reasoning. But as alternative investments grow in popularity, that approach is becoming harder to defend. A structured, goals-based process is essential to ensure allocations are not only suitable for each client, but also aligned with their objectives, timeline, and liquidity needs.

The core issue is not just about access to alternatives, it is about how those allocations are determined, sized, and supported. As private assets move from the margins to the mainstream, firms need a more disciplined way to connect these complex investments to each client’s real-world goals and constraints. That means moving beyond gut feel and static models to a framework that accounts for liquidity, timeline, and portfolio interdependencies.

Our framework enables that shift. We support modeling illiquid assets within a broader portfolio context, helping advisors size allocations appropriately based on each client’s goals and liquidity profile. The platform also enables allocation to interval funds and other semi-liquid strategies, while flagging the trade-offs in terms of access, risk, and redemption features.

In this emerging space, advisory firms that rely on guesswork, or lack a documented process, are especially vulnerable. We believe our structured approach provides both improved client outcomes and stronger regulatory protection.

Model Portfolios Are Not a Panacea

Many firms have adopted model portfolios to improve efficiency and scale and to attempt to remedy the “rep as PM” approach. But models alone do not solve the compliance challenge. While mapping a risk score to a model may appear systematic, such an approach often oversimplifies the client’s needs and fails to demonstrate alignment with their financial goals, exposing firms to both regulatory and business risk.

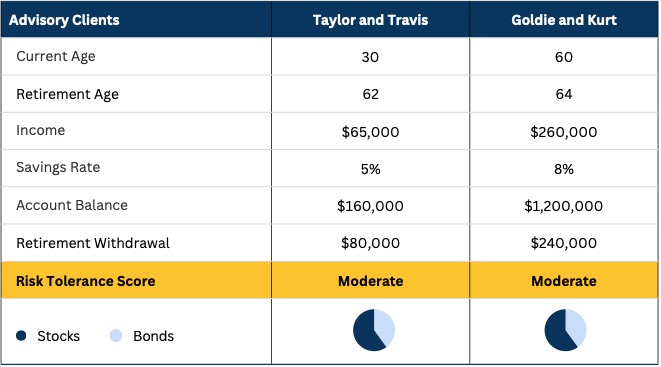

Consider this common scenario: an advisor, Lionel Richie, has two clients: Taylor and Travis Swift and Kurt and Goldie Hawn. While they share a flair for showbiz, that’s where the similarities end. The Swifts are young, still accumulating wealth, and focused on saving for a long-term retirement. The Hawns, on the other hand, are nearing retirement, with more assets, more income, and a desire for stability and income preservation.

Yet there’s one unfortunate thing they have in common: both scored a 60 on a risk tolerance questionnaire taken on a random Tuesday afternoon.

So, Lionel, following firm policy, places them both in the same “moderate” model portfolio. He then runs a probability-of-success analysis, sees that both clients are projected to exceed an 80% success rate, and considers his job done. The plan appears viable, so he implements and moves on without ever reconciling whether the portfolio truly reflects the distinct financial lives and goals of each client.

Lionel can even go through a lengthy financial planning process capturing their time horizon, savings rates, cash flow needs in retirement, goals and legacy wishes. But this detailed financial plan is ultimately disconnected from the investment recommendation. At the critical moment of aligning portfolio strategy with financial outcomes, all that valuable planning insight is sidelined. The clients’ unique goals become secondary to a standardized risk score. This isn’t just a missed opportunity for personalization, it’s a compliance vulnerability.

For illustration purposes only.

If regulators ask why clients with radically different profiles are in the same portfolio, Lionel (and his firm) may struggle to defend the decision because they lack documentation of a goals-based rationale – just a risk score and a default model. That’s not a process that is likely to stand up well to scrutiny.

The business risk is just as real. If the Swifts or the Hawns don’t understand why they’re in the portfolio they’re in, they’re far more likely to leave, especially after a market downturn. As one advisor put it: “A client who doesn’t understand the outcome they’re investing toward is a client who won’t stick with the plan. ”

Advisors and firms alike have seen it time and again: clarity and connection increase understanding and reduce emotional reactions. This potent combination leads to better investment decisions. Model portfolios can be part of the solution, but only when integrated into a broader, goals-based framework that treats each client’s needs as unique and worth tailoring to.

Conclusion

Our process gives firms a systematic way to connect each client’s unique goals, risk tolerance, cash flows, and time horizon to either a bespoke portfolio or an optimal model from a suite of firm-approved options. This gives advisory firms a scalable framework that improves client outcomes while materially reducing firm-level compliance risk. Key benefits include:

- Consistency across the organization: Standardized processes that reduce variability in advisor practices

- Documentation and defensibility: A clear rationale for each investment decision that can be logged in CRM or compliance systems

- Supervisory clarity: The ability to demonstrate oversight of asset allocation and portfolio construction decisions firmwide

This process may not solve every compliance issue. But it can give your firm a clear, auditable process to answer the regulator’s most important question:

“Why is this client in this portfolio?”

And in today’s environment, that may be the most important answer your firm can provide.

- Michelle Atlas-Quinn, J.D., “Don’t Be a Statistic: 10 Compliance Fails That Can Sink Your RIA, ” Advisor Law, June 21, 2024. ↩︎

- Winston & Strawn, “OCIE Identifies Common Compliance and Supervisory Deficiencies of Investment Advisors, ” Client Alert, December 2020. ↩︎

- See “The Perils of Outsourcing Asset Allocation to a Risk Score, ” Nebo Wealth, June 2024 and “Risk Scores – Putting the Horse Behind the Cart, ” Nebo Wealth, August 2024. ↩︎

- Survey results based on hundreds of advisor responses conducted by Nebo Wealth in 2023 and 2024. Negative response includes no and not sure. ↩︎

- “The False Choice in Portfolio Construction, Building Blocks, and the Advisory Solution of the Future” Vestmark, page 2, December 2019. ↩︎

- All advisor quotes are anonymized and reflect direct feedback captured during meetings with RIA and enterprise firms. They are presented to illustrate representative sentiment and not the views of any specific individual or firm. ↩︎

- “SEC 2024 Examination Priorities Indicate Increased Scrutiny of Investment Advisers and Continued Focus on Cybersecurity, FinTech, and Anti-Money Laundering Programs,” O’Melveny & Myers, LLP, December 2023. ↩︎

- “The State of Alternative Investments in Wealth Management, ” CAIS-Mercer, 2025 Report, Exhibit 7: Challenges for Financial Advisors in Adopting Alternatives. ↩︎

GET TO KNOW NEBO WEALTH

Nebo Wealth is a leader in goals-based investing and personalized portfolio construction. Powered by award-winning wealth optimization, it’s how advisory firms elevate the value of their advice, deliver more personalized, goals-driven portfolios, and seek to achieve better outcomes for their clients and their practice.

After a decade of research, Nebo Wealth launched in 2022 and has been recognized with numerous awards, garnered praised from industry leaders, and become a leading provider of goals-based investing solutions for advisors.

READY TO LEARN MORE?

Visit us at www.nebowealth.com to learn more or schedule a brief exploratory call and interactive demo.

IMPORTANT DISCLOSURES

The views expressed represent the opinions of Nebo Wealth, a division of GMO, LLC. which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Nebo Wealth believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability.

This presentation is for general information and education only. Nebo Wealth makes no representations or warranties in respect of this presentation and is not responsible for the accuracy, completeness or content of information contained in this presentation. Nebo Wealth is not responsible for, and expressly disclaims all liability for, damages of any kind arising out of use, reference to, or reliance on any information contained in the information.

Nothing in this presentation should be construed as an offer, or solicitation of an offer, to buy or sell any financial instrument. It should not be relied upon as specific investment advice directed to the viewer’s specific investment objectives. Any financial instrument discussed on this webpage may not be suitable for the viewer. Each viewer must make his or her own investment decision, using an independent advisor if prudent, based on his or her own investment objective and financial situation.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money.

Copyright © 2025 by Nebo Wealth, a GMO LLC Company. All rights reserved.