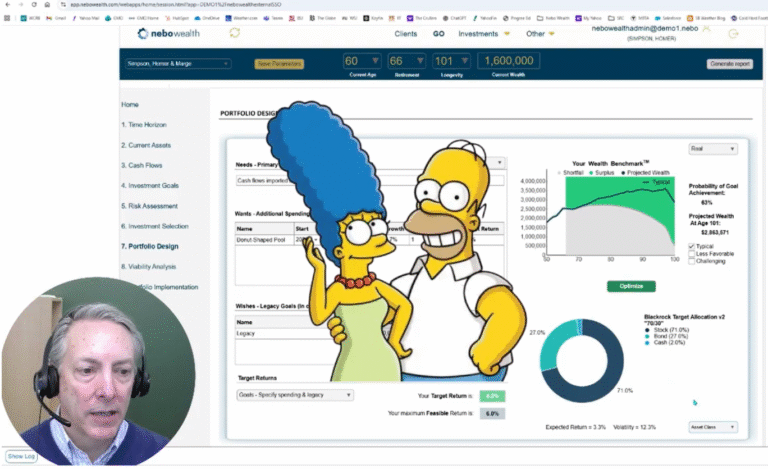

The Dangers of Relying Too Much on a Risk Score

Here’s a simple test: Is this portfolio tied to the client’s time horizon and cash flows, or just their comfort with volatility?

A 25-year-old should invest aggressively because of her circumstances, not her personality. She has 40 years until her drawdowns really matter for her consumption goals.

A 75-year-old should invest more conservatively because of her needs and circumstances e.g. her near-term losses can’t necessarily be recovered from her nest egg as it is being consumed.

Yet both of these clients can end up in a 60/40 portfolio if they have the same risk score. Using a risk score to build a client portfolio essentially nullifies an advisor’s great financial planning, throwing all that work out the window. The resulting portfolio is completely disconnected from the client’s financial plan.

P.S. There’s a lot of attention on advisor workflow right now, which makes this point increasingly relevant Martin Tarlie